OUR PERFORMANCE

CIO'S BUSINESS REVIEW

Equities

The equity portfolio generated a return of a negative 4.8% during the year ended 30 June 2023. This was primarily driven by forex and capital losses in the Kenyan market due to a challenging macro environment post-election. Following the election of H.E William Ruto, tough measures intended to improve the fiscal position were taken that initially caused unrest and resistance. These include the Finance Bill of 2023 which eliminates subsidies, doubles VAT on fuel to 16%, increases to tax rates for high-income earners and reductions in current recurrent and capital expenditure.

As a result, protests were held which spooked investors while inflationary pressures from global conditions meant the country was in a tough position to implement new measures. Consequentially, the NSEASI suffered price depreciations as foreign investors became net sellers on the country’s macro issues and negative sentiments around possible spikes in NPLs in the banking sector and Safaricom’s challenges in Ethiopia. As an index, the NSEASI lost 14.04%. In local currency with notable losers Safaricom (30 percent) and KCB (2%) while the forex loss of 22.22% exacerbated the loss to over 34%.

Despite the Kenyan situation, the Fund’s equity portfolio losses were cushioned by Tanzanian counters that returned 14.9% due to attractive dividends and capital gains from CRDB (28%), NMB (20%) and TWIGA cement (17.5%) and associates that returned 15% due to good dividend yields from UMEME and Housing Finance Bank justifying the Fund’s diversification strategy across different countries and sectors in the equity markets.

Real Estate Portfolio

We hold real estate assets to realise capital gains and earn income. Over 70% of this asset class comprises undeveloped land.

The strategy is to continuously work towards unlocking the value of some of the prime land through either, commercial developments for rent or the sale of residential units.

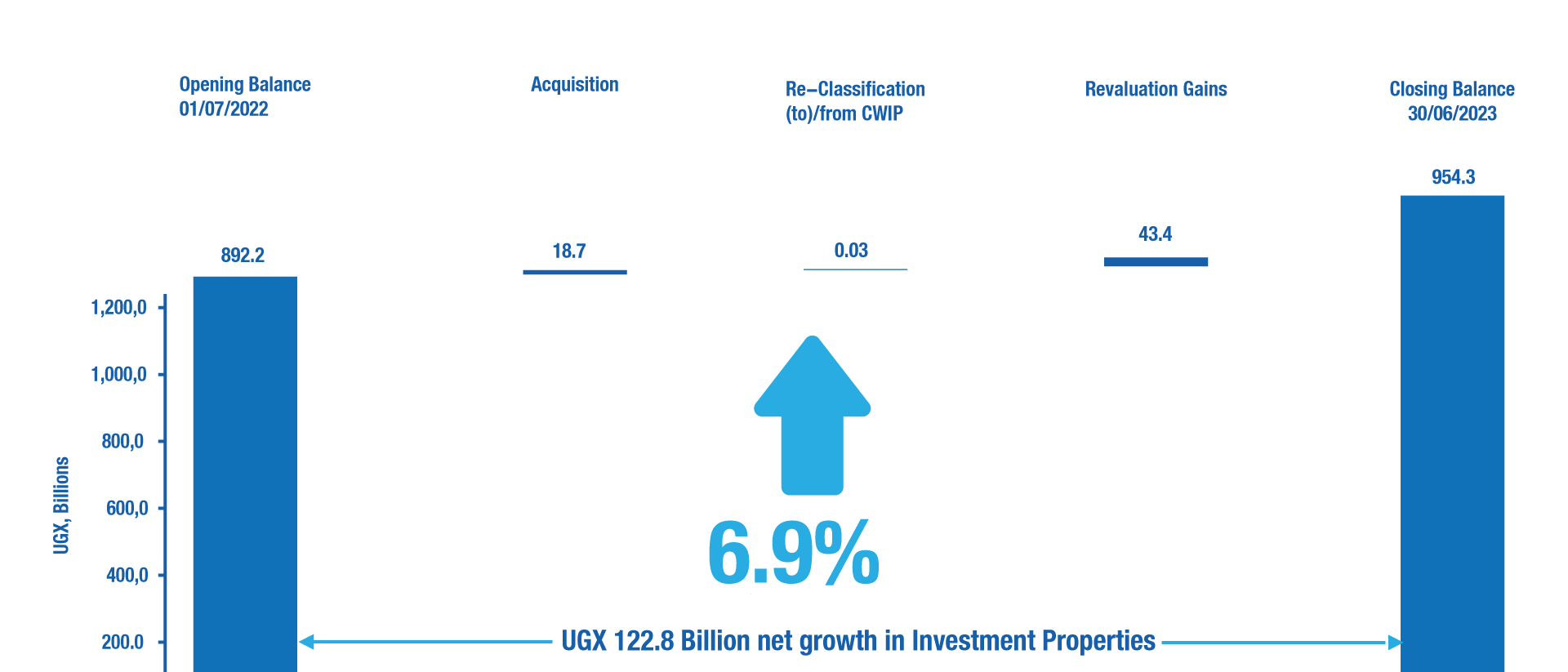

The entire real estate portfolio (including non-income generating assets) yielded 5.70% during the financial year to June 2023 which is the same that was recorded last year. This return is mainly attributed to capital gains and sale of residential housing units.

The illustration alongside shows the build-up of the investment properties for the financial year ended 30 June 2022

Figure 8: The growth in the Fund’s Investment Properties over the last year

Source: Internal

Real estate project information update

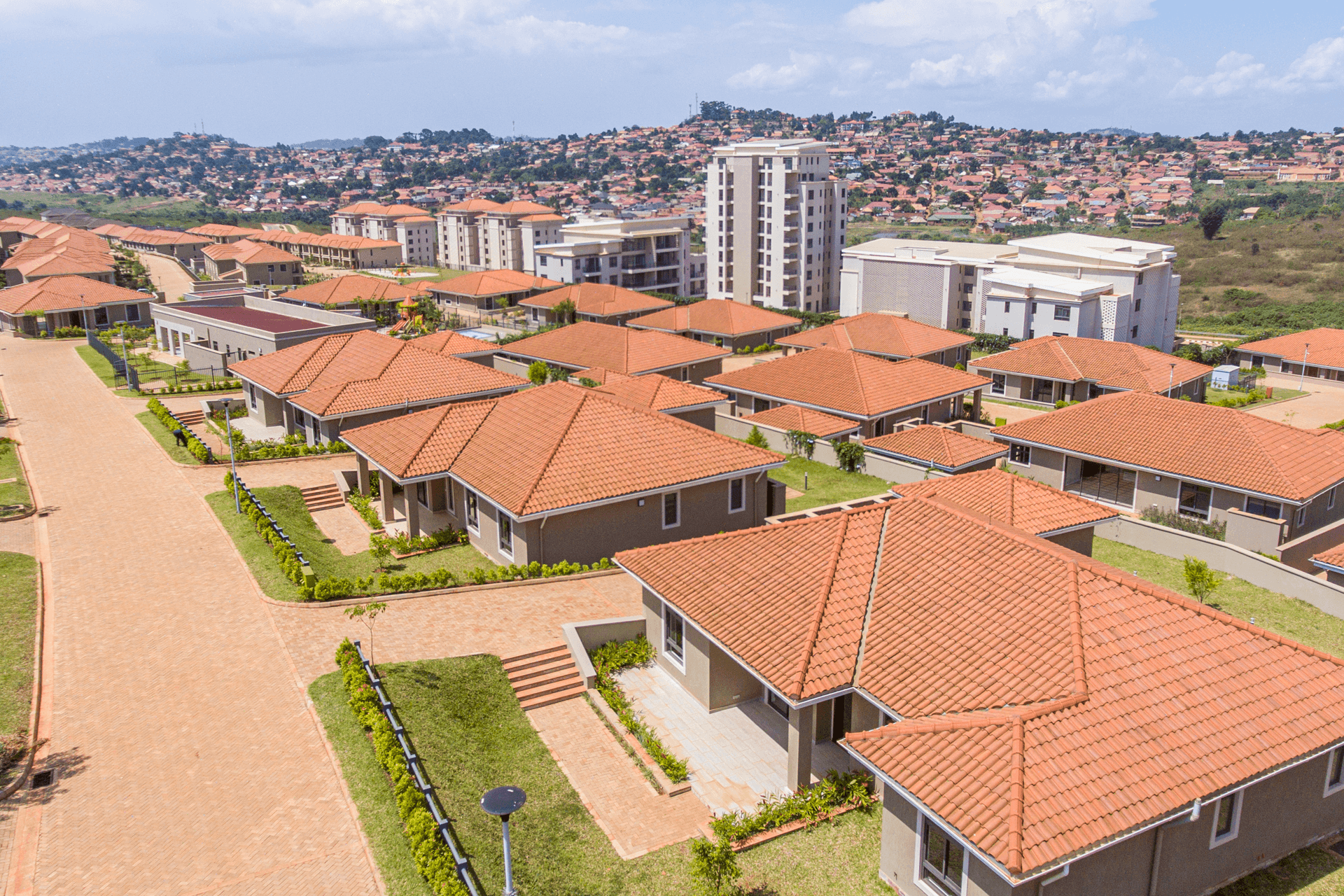

Lubowa Housing Project

The Lubowa Housing Project is conceptualised as a self-sustaining satellite city with mixed-use housing and commercial developments on approximately 600 acres. The project is intended as a phased development with construction starting with an initial 306 housing units on 78 acres. Phase 1 will comprise of four (4) distinct house types: Apartments, Bungalows, Townhouses, and Villas.

The progress so far:

Construction works for all house types were completed by 30 June 2023. We have since commenced selling and the market response has been excellent.

Temangalo Housing Project

This project is expected to have 3500 units when completed. Phase one is currently under construction and is sitting on about 70 acres.The progress is about 48%. It will have 10 house types.

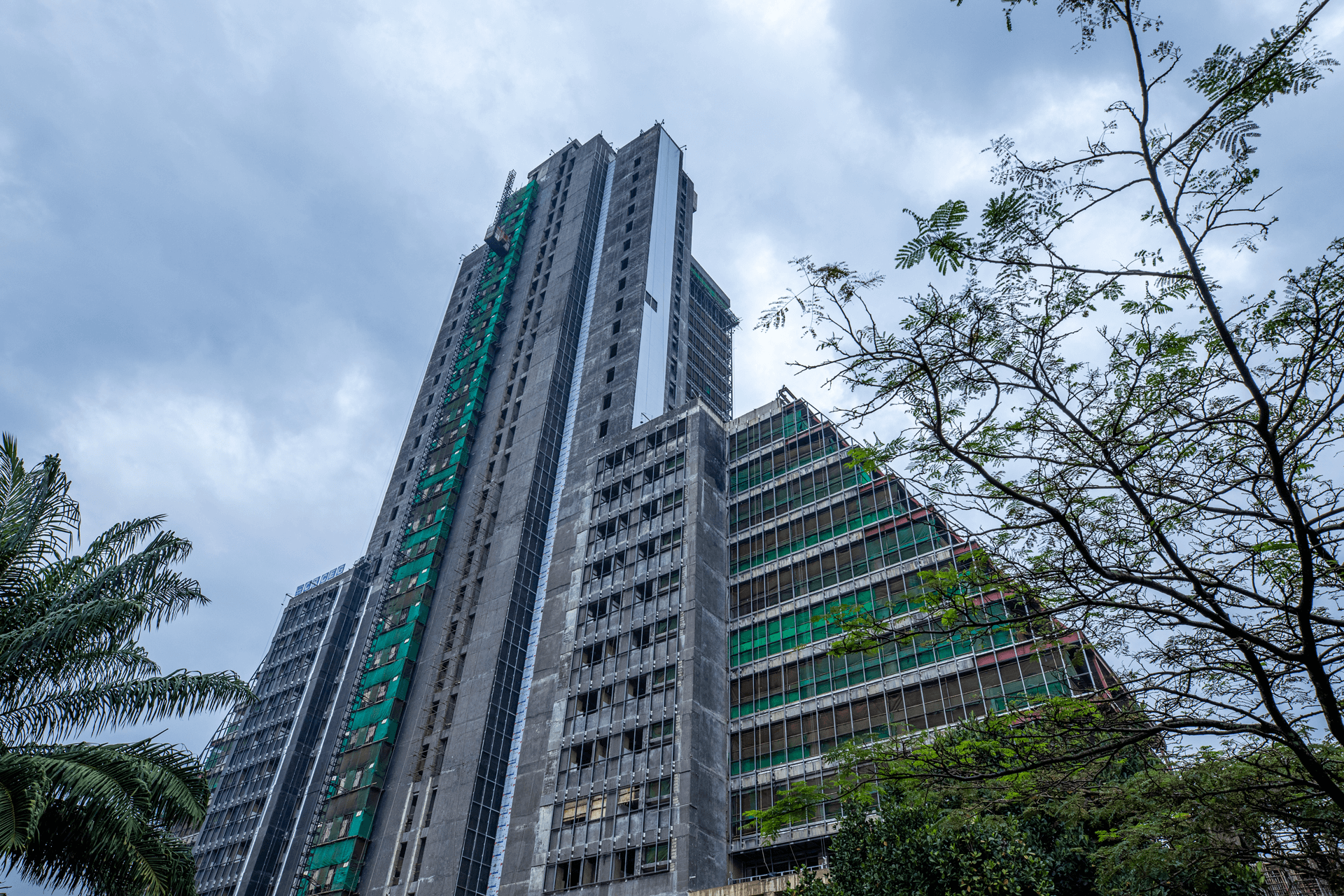

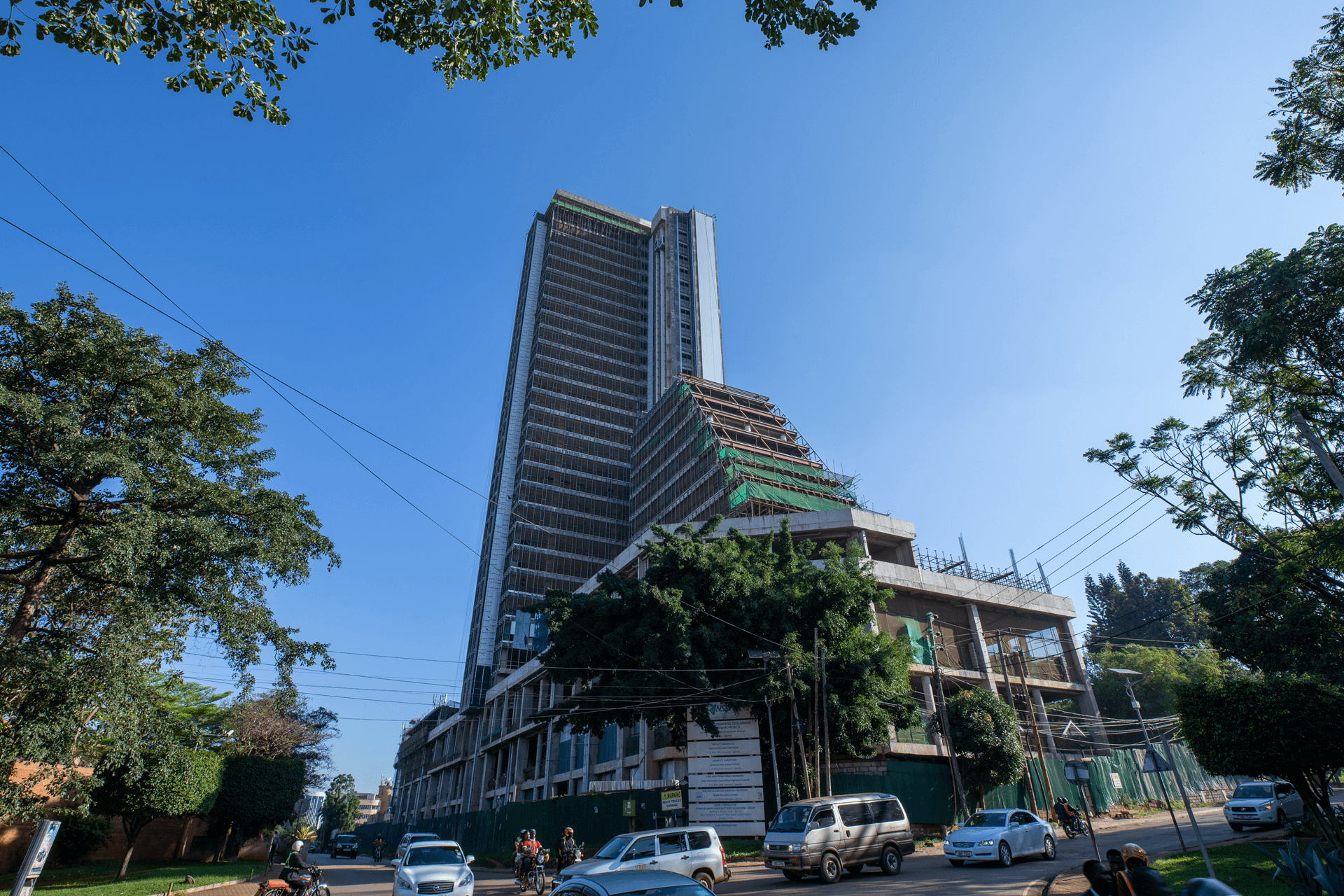

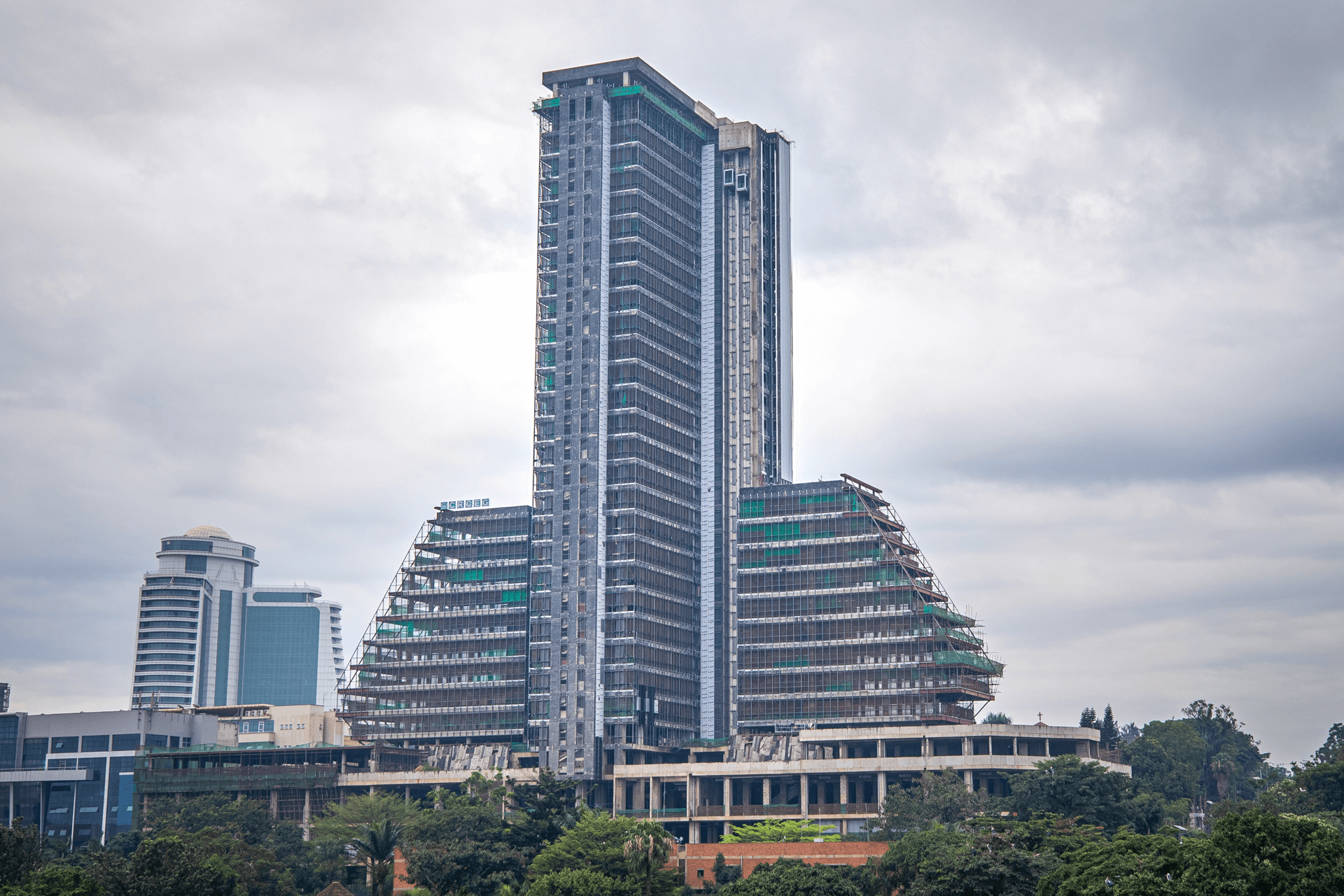

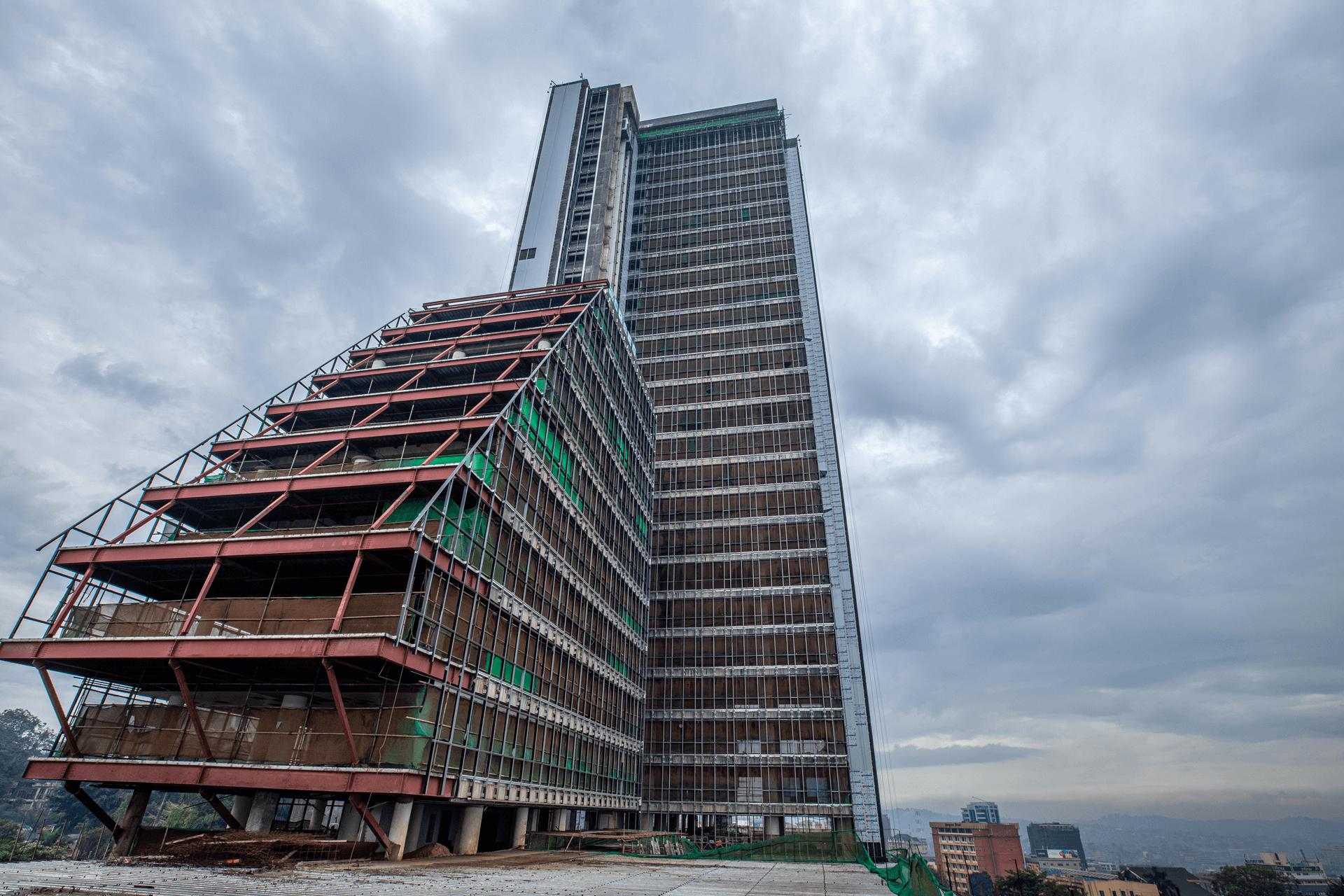

Pension Towers

Pension Towers is conceptualised as an intelligent and modern commercial complex comprising 3 Towers (with a height of 32 floors) all sitting on four basement floors for parking. The total built-up area will be approximately 75,000m2 that will house office and retail space. The project has frontage on both Lumumba Avenue and Nakasero Road.

The progress so far:

Construction works are ongoing and as of 30 June 2023, the progress was estimated at 80%.

2023/2024 Outlook

We intend to continue with portfolio rebalancing. For the fixed income asset class, this will be done by exploring corporate bonds and structured product opportunities. We will also continue to seek more diversification opportunities within Uganda and the East African region.

In the equity asset class, we will explore opportunities in all the markets where we invest. Private equity also remains high on our radar.

In the real estate asset class, the strategy is to continuously work towards unlocking the value of some of the prime land through either undertaking commercial and mixed-use developments for renting out or building residential houses for sale. A total of 70% of the real estate class comprises undeveloped land. Developing the land is one of the ways of unlocking the accumulated value over time.